Accounting is a language that helps us to understand the financial status (profitability and position) of an organization. When we study this, it encourages us in flourishing a new skill in a specialized field.

It enhances us that we can communicate and understand the financial position and profitability of a business.

It allows any business to understand its financial position and profitability. They can understand how their organization stands in a market.

Nowadays, running a business without this is like traveling without any objective. This implies we cannot compete in a modern world without computing profits and losses and that can be only done with access to proper accounting.

It is a systematic process of identifying, recording, measuring, classifying, verifying, summarizing, and communicating financial information i.e. in terms of money of a company.

What You will get:

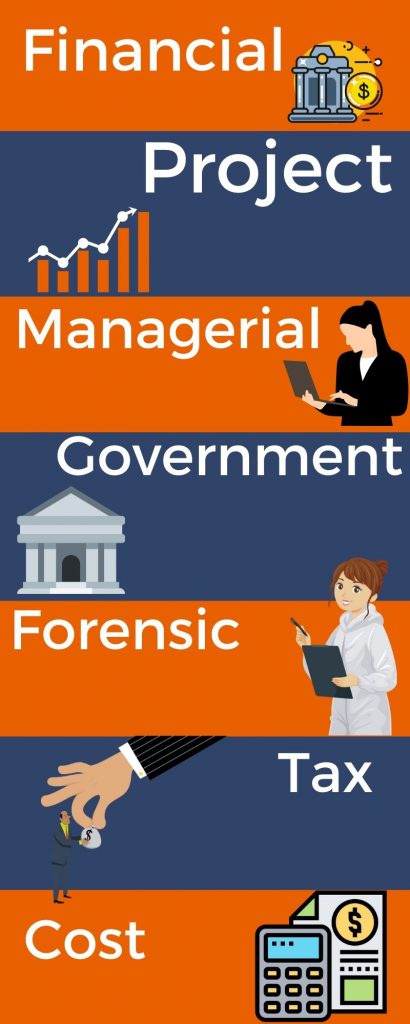

Types of bookkeeping:-

1. Financial accounting: –

It refers to the process of collecting and preparing financial information of organizations known as financial statements.

For example: Balance sheet, P&L Account, cash flow statement etc. These are further used by shareholders which led them to know about the financial position and profitability of company.

2. Project accounting:–

This type is specially needed for projects. It is used by the organisation for creating the financial reports which are specially designed to drag the financial performance of projects which are further used by project managers.

This allows helps management to see all the costs, resources, etc. of projects. It helps them to analyse the information like budget etc.

3. Managerial accounting:-

This provides information to management which helps them to take decisions regarding the growth of the company. It is only used for internal objectives.

“It refers to process of creating reports and documents which supports management in decision making process for consistent flow of company.

4. Government accounting:-

“It refers to the process of recording, analyzing, classifying, summarising, interpreting, financial data which are related to government expenditure, revenues, and throwback all information” Oshisami and Dean.

It is based on double entry system.

5. Forensic accounting:-

“It refers to the utilization of skills to investigate fraud or embezzlement and to analyze financial information for use in legal proceedings.”

Forensic accountants learn some techniques and skills to catch the fraud from the company.

For example, Some companies do not record some transactions to get rid of the tax, so that, at that time we need that accountant who observes all transaction to find out the fraud.

6. Tax accounting:-

“It refers to the process of preparing tax returns and planning for future taxable payments of a company”.

This accounting does not focus on all transactions of the company but only analyze the transactions which affect the tax charge.

Its principles is also differs from GAAP (principles). Its main work is to generate taxable income figure from income figure of an entity.

7. Cost accounting:-

“It is the process of recording, classifying, analyzing, summarising, allocating costs associated with the process and then developing various course of action to control the cost and improve management”.

Let’s understand with an example, A ltd. Produce pens and it cost them 10rs. But after some time they find that now pen costs them for 12rs. They get to know that their cost rises due to direct material i.e. raw material. So now they can take steps regarding the cost with the access of cost accounting.

Characteristics:

As we know that features of anything are always hidden in its definition. In that way features of this concept also hidden in its definition:

- Recording

- Classifying

- Summarising

- Interpretation

- Communication

Let’s understand these features in brief:

1. Recording:-

Primary function is to record all the transactions. One thing also kept in mind that, only those transactions recorded in the books which are monetary transactions or which can be measured in terms of money.

There are many transactions that are very essential for the organization but cannot measure in money. So it will not be recorded.

For example, the quarrel b/w production manager and sales manager, a strike by employees, etc. Though these events affect the entity but cannot be measure in money. So it will not be recorded.

2. Classifying:-

After recording the transactions in journal or subsidiary books, these are classified.

Classification refers to process of grouping the same nature of transaction at one place in a separate account.

Separate accounts are opened in the ledger in the name of each person, whether the customer or seller. Also separate accounts are opened for purchases, sales etc.

This same treatment also done for all expenses that are already recorded in the journal.

3. Summarising:-

It refers to art of presenting the classified data in such a way which can be understandable and useful to management and other users of such data.

It including matching of all ledger balance and preparing trial balance (balance of all ledger accounts).

Trial balance includes Trading and P&L Account and a Balance sheet. Trading account is prepared to know gross profit or loss, P&L a/c is for net profit or net loss.

Balance sheet is prepared to know the financial position of an entity.

4. Interpretation:-

In Business, the results are presented in such a manner (i.e. by preparing Trading and P&L account and balance sheet) so that the parties take interest in the business.

These parties include investors, public, bank, employees. They can have full information about the business in the way of profitability and financial position.

5. Communication:-

Its features also include the communication of financial data. This data is presented to users, according to the requirements. It cannot be done without communication.

For example, Investors analyse that information to invest in that business for the motive of profits, also bank use financial position to check the position of an entity for a loan as they can repay or not.

Why it is needed ?

After the end of each year, all the businessmen want to know how much they have gained or lost during the year, how much is capital is invested in the business at the end of the year, how much amount they are liable to pay and to whom the owe it, how much is owed to them and by whom etc.

In order to attain such information, it is mandatory to keep a complete and systematic record of each and every business transaction entered into during the year.

We all hear that it is important but we have to think that, why is it important?

Lets discuss about the some importance:

1. Helps in growth:-

When we buy something and before the buying, we look after some samples and reviews and after that we decide about the buying or not.

Likewise, every investor needs the financial statements to know about the stats of company and this can be only possible by accounting. So that, maintaining accounts can help an entity in growth.

2. Reduce expenses:-

With the access of this, an organization can mirror its all expenses so that they can track the overspending if there is. Hence, they can control their cost.

3. Budget and future need:-

Sometimes enterprises think to increase their capital in the future, but if they do not know about their current stats whether profit or loss, then they can not expand their business.

So a business can plan the growth and budget only if they had their financial statements.

4. Helpful in assessment of tax liability:-

Properly maintained accounts will be a great help when the firm is assessed to income tax or gst ( sales, purchase etc.)

These maintained records are trusted by maximum taxation authorities.

Conclusion

At last, we can conclude that the importance of accounts is increasing day by day and also the scope of accountants.

Now, the properly maintained accounts can give the answer of a number of questions such as:

- What is the cost of production.?

- Is this reasonable or not.?

- Can it be reduced and if so, in what manner.?

- What should be the selling price based on the cost of production.?

Thus business owners can take important decisions with the help of information provided by account data.

Also if you do accounting with interest, then you can do what ever you want, because its like a weapon which can be used in any career.

Frequently asked questions

Ans: Italian Luca Pacioli, described the concept of bookkeeping in 1494.

Ans: Mainly Tally and Busy software is used in India.

Ans: These Standards in India are issued by the Institute of Chartered Accountants of India (ICAI)

Ans: This is the period of time over which a company gathers and organizes its financial activity

Content Marketer

{kind=link}