In this modern era, most of the business transactions are made on credit. In this case, Purchaser promises to the seller for the payment with the concerned due date. (Bills of exchange)

But, sometimes the seller does not believe on the buyer because of some previous operation and he would like to get that promise in a written form that is authorized by the government.

In case, the buyer does not make a payment on due date, the seller can take lawful action against him with the help of that note known as Bills of exchange.

According to Indian negotiable Instrument act, 1881:-

“A Bill of exchange is an instrument in writing, an unconditional order signed by the maker directing to pay a certain sum of money only to or to the order of a certain person or to the bearer of the instrument.”

What we will learn:

- Parties involved

- How it works

- Promissory note

- Discounting of Bill

- Negotiation of Bill

- Endorsement of bill

- Retiring the bill under Rebate

- Dishonor of Bill

- Renewal of a Bill

- Conclusion

- Frequently asked questions

Indian Negotiable Instrument act, 1881 govern all such instruments.

As the Bills of exchange is an instrument of credit purchase and sale which makes easy the credit sale of goods. These are known as ‘Hundis’ in India. These are written in Indian language

But in western countries, the name of these instruments called ‘Promissory note’ and ‘Bills of exchange’. But these two terms differ from each other.

Features:-

- It must be in written form.

- The payment date should be fixed.

- It contains an order, not a request.

- These should be authorized by the government in the form of stamp stuck on paper.

- Maker and acceptor must sign this.

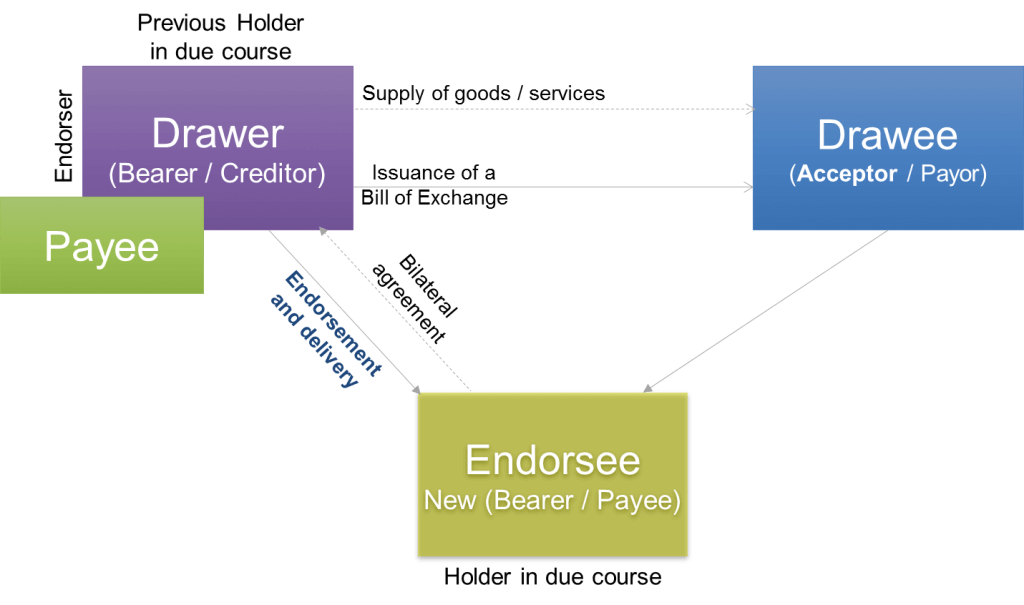

Parties involved in Bills of exchange:

Drawer:

He is the seller or creditor who is entitled to receive money from someone. He writes the bill or draws the bill as Drawer and signs on the Bill to validate.

Drawee or Acceptor:

He is the person who purchases goods and for whom, the Bill is prepared and he is liable to pay the amount mentioned in the bill. He accepts the bill by writing ‘accepted’ and then signs it.

A bill is called draft before drawee accept.

Payee:

It refers to the person to whom the payment to make. The Drawer or seller can be payee only if he retains the bill with itself until the date of maturity.

If Drawer endorses or transfers the bill to a third party, then the payee will be that party. Banks can also become a payee if a drawer or third party discounted that bill from the party.

Payee consider bills as assets.

How Bills of exchange works:

Let’s understand with example,

On 1st July, Ramesh sells goods to Sanjeev costing 1,00,000 on credit. The payment time is after 2 months. Ramesh prepares the bill on Sanjeev who accepts it and returned to Ramesh.

But, Kaushal one of the seller of Ramesh, had to receive payment from Ramesh rs.1,00,000, and Ramesh transfer that bill to Kaushal.

In this case,

| Drawer: Ramesh |

| Drawee: Sanjeev |

| Payee: Kaushal |

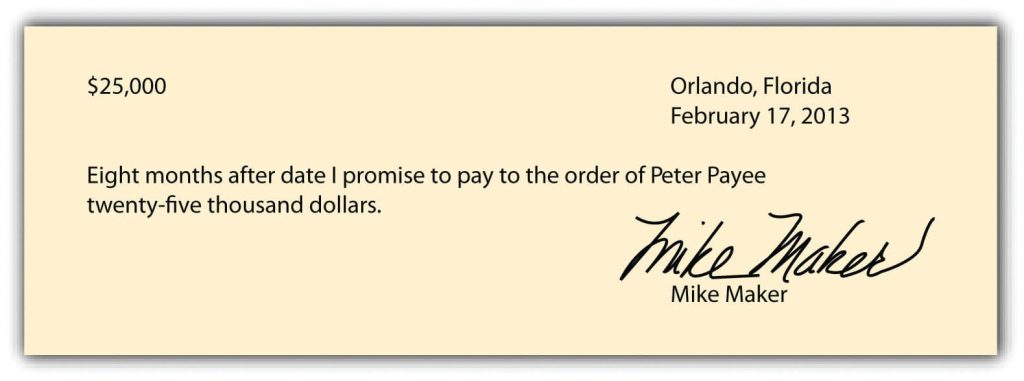

Promissory Note:

Sometimes, the Buyer feels uncomfortable for the purpose of credit and then he himself prepares a note, signs it, and gives it to the seller, called ‘Promissory note’.

According to Indian Negotiable instrument act, 1881

‘It is an instrument in writing containing an unconditional promise signed by the maker to pay a certain amount of money to a certain person.’

Features:

- It must be in writing.

- There must be a promise to pay money not order.

- The amount must be specified.

- It must be stamped according to its value.

Parties of promissory note:

- Maker: – He is the person who prepares promissory note and signs it.

- Payee: – He is the person who is entitled to receive payment.

From the above example, we assume that Sanjeev himself writes a bill promising Ramesh to pay 1,00,000 and signs and give to the seller.

In this case,

| Maker: Sanjeev |

| Payee: Ramesh |

Difference Between Bills of exchange and Promissory notes:

Date of Maturity: The date on which payment of bills becomes due I called ‘due date’ or date of ‘maturity’

Date of grace: While estimating the due date of the bill, it is mandatory to add an extra three days to the period of the bill, called ‘Date of grace’.

For example, if the due date of a bill after 3 months is 1st September, then its maturity date will be 4th September.

Notes*

- If the due date (including the days of grace) falls on Sunday or any public holiday, the due date will be one day earlier. For instance, if the due date falls on 26th January, the payment will be on the 25th.

- If the due date (including grace days) declared as an emergency holiday, the payment will be made one day after.

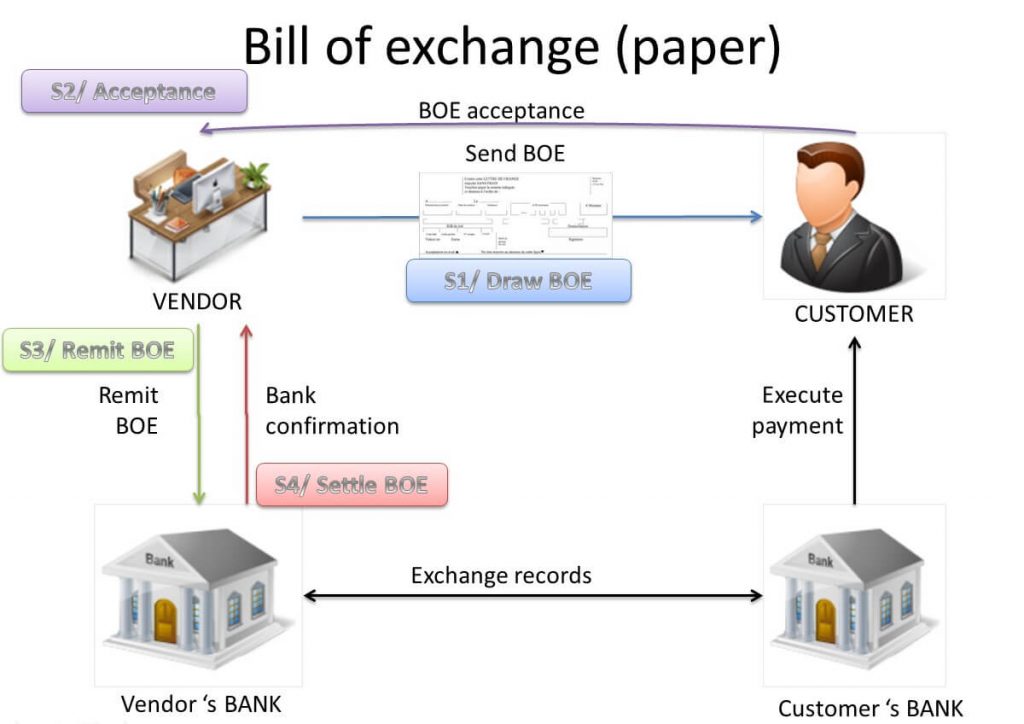

Discounting of bills of exchange :

Sometimes, the holder of B/R needs money before the date of maturity, then he has a facility that he can discount bill from bank.

In other words, He can collect money from the bank by depositing that bill to that bank. In response to this, Bank charges some fee which it deducts from the actual amount and pays the residual amount to B/R holder.

These charges can be termed as interest. At the date of maturity, Bank collects complete payment from the Drawee.

Negotiation of Bills:

It means the transfer of bills of exchange to another person in such a manner that the transfree (who receives bills) becomes the holder of Bill and have the right to make the bill on his own way.

Now, He can recover the amount from the concerned person.

Modes of negotiation:

- By delivery: If the bills of exchange are payable to bearer, it may be negotiated by delivery and does not require the signature of the person to whom this instrument is transferred.

- By endorsement and delivery: When the bill is already specified to pay to that person or to his order, it can be negotiated only endorsement and delivery. An endorsement is signing the bill for negotiation.

Endorsement of a Bill:

It means signing the bill for the purpose of negotiation. In this case, a B/R holder can transfer that bill to another person by signing on the back of the bill. The person transferring the bill is called ‘endorser’ and who receives the bill known as ‘endorsee’.

Now, the endorsee has also had to right to endorse that bill to another person by doing the same person. The person holding the bill until the maturity is entitled to receive the amount.

Retiring the bill under Rebate:

Sometimes, the drawee makes the payment before the due date which is called retiring bill under rebate. In this case, the holder allows them some discount for the early payment. This discount is termed as ‘Rebate’.

This rebate is a gain for drawee and an expense for the holder. Such rebate is calculated specified rate per annum for the period of payment is made early.

Dishonour of a bill:

Sometimes, the acceptor or drawee of the bill refuses to pay the amount on the maturity date or becomes insolvent, called dishonor of the bill.

For the recovery purpose, the holder of a bill must give a notice to which he seeks to make liable for payment.

Such notice must be served immediately after dishonor or within a certain time. If this is not done, the drawer loses the right to recover the amount.

Noting charges:

To make the case stronger, the bill is usually handed to the person called ‘notary public’, which is appointed by the government.

The notary public again presents the dishonored bill to the acceptor of the bill and if he still refuses to make the payment, the notary public verifies the facts of dishonor on the bill by itself.

This act is called noting. For this, they charge some fee for referring such services known as ‘noting charges’. Firstly, the holder of the bill pays the notary charges but afterward recover from the acceptor.

Renewal of Bill:

Sometimes, the acceptor finds himself unable to pay the bill on the due date and requests to the drawer to cancel the old bill and to make a new bill in place of the older one.

If the drawer agrees, a new bill is drawn for the original amount or for the rest of the amount if acceptor paid some amount.

Holder also charges some interest for the inconvenience and receive that amount in advance or adds that amount in that bill.

Conclusion

From the above explanations, we can conclude that the Bills of exchange had made the business easy.

Now, A businessman can purchase and sell goods on credit very securely. Also, this play is an essential role in Accounting.

Frequently asked questions

Ans: Arab merchants used a similar instrument as early as the 8th century ad, and the bill in its present form attained wide use during the 13th century among the Lombards of northern Italy, who carried on considerable foreign commerce.

Ans: A letter of credit is an agreement in which the buyer’s bank guarantees to pay the seller’s bank at the time goods/services are delivered. The main difference between the two is that a letter of credit is a payment mechanism whereas a bill of exchange is a payment instrument.

Content Marketer

{kind=link}