Advance ruling means an opinion by the authority in relation to transaction which has been undertaken or is proposed to be undertaken by an assessee.

He makes an application on issues where he is facing a difficulties.

Case scenario:-

MR. Donald trump of united states of America has come to India and earn a certain income. This income taxability has not been specified under the income tax act. So for obtaining the tax rate applicable to him, he makes an application to advance ruling.

Thus through advance ruling he will be able to know his tax rate.

What you will get?

- Definitions.

- Authority for advance ruling.

- Applications for advance rulings.

- Applicability for advance rulings.

1. Definitions section245(Na):-

- Section 245 N(a)(1) in relation to a transaction has been undertaken or is proposed to be undertaken by a non-resident application.

- Section 245 N(a)(2) tax liability arising of a non-resident in respect of transaction under taken by a resident applicant with the non-resident.

- Section 245 N(a)(2a) tax liability of a resident applicant in respect of a transaction undertaken or is proposed to be undertaken and such determination shall includes a question of law or question of facts.

- Section 245 N(a)(3) in respect of an issue which is related to total income and is pending before income tax authority or appellate tribunal and any question of law or question of fact is pending on such application.

- Section 245 N(a)(4) decision in respect of which transaction has been undertaken or is proposed to be undertaken which is impermissible avoidance arrangement (IAA).

**Applicant may be any person who is a,

- Non-resident or,

- Resident or,

- Resident of such class or category as central government may satisfy or,

- Resident falling under such category which has been classified by central government in the official gazette or,

- Referred to in Section 245NA(4).

2. Authority for advance ruling (AAR): –

Composition of authority for this ruling : –

- AAR to appoint a chairman, vice- chairman, revenue member and law member as the central government may give an approval.

- Chairman should be a judge of the supreme court or the chief justice of the high court or judge of the high court for at least 7 years.

- Vice- chairman should be a judge of the high court.

- Terms and conditions of services and salary payable to the members are such as may be prescribed.

- Location of AAR: – National capital territory of Delhi.

- Composition of benches: – there should be 1 chairman, 1 vice chairman, I revenue member board and 1 law member board.

- Any vacancy of the chairman arises due to death, resignation or otherwise than the senior most vice- chairman will act as a chairman.

- Location of the benches will be at all such places as central government may specify.

Qualifications, terms and conditions of service of chairman, vice chairman and members: –

- Power of central government to make rules of terms and conditions, qualifications, appointments, salaries, resignation and removal.

- Terms of chairman, vice- chairman and members are of not more than 5 years.

- Age criteria of chairman, vice- chairman and members are,

70 years for chairman

and,

67 years for vice- chairman and members.

3. Applications for advance rulings: –

An applicant desirous of obtaining a ruling may make an application to AAR.

Fees of Rs. 10000 should be paid for making an application .

In case application is made in respect of section 245NB(1)(2) (2a) than fees will be ,

- Rs. 200000 where amount of one or more transaction does not exceed Rs. 100 crores.

- Rs. 500000 where amount one or more transaction does not exceed Rs. 300 crores but exceeds Rs. 100 crores.

- Rs. 1000000 when amount of transaction exceeds Rs. 300 crores.

Every application made should show a proof of payment of fees.

Within 30 days of making an application if an applicant want to withdraw an application, than he may also withdraw an application.

For referring case laws on this ruling you can visit a website whose link has been given below,

https://www.taxmanagementindia.com/visitor/case_laws_list2.asp?Law=17&court=AAR

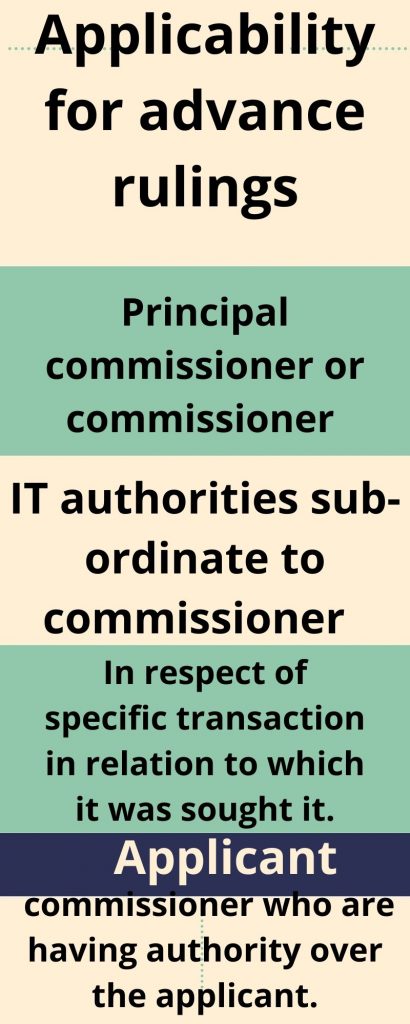

4. Applicability for advance rulings: –

The application on this ruling shall be binding on,

- Applicant who has sought it.

- In respect of specific transaction in relation to which it was sought it.

- On the Principal commissioner or commissioner and the income tax authorities sub- ordinate to commissioner or commissioner who are having authority over the applicant.

An advance ruling shall be continue to remain applicable unless there is a change in law or in fact in relation to circumstances of which the advance ruling was pronounced.

Vacancies, etc not to invalidate proceedings section 245 (P): –

No proceeding before or after the proceeding of this ruling shall be questioned or shall be invalid on the ground merely of the existence of any vacancy or defects in the constitution of the authority.

Advance ruling to be void in certain circumstances : –

When an advance ruling has been obtained by fraud or misrepresentation than the said order shall be considered as void ab initio .

The provision will be applicable to applicant as advance ruling order was never made . A copy of this order will be sent to applicant , principal commissioner or commissioner.

You can Visit my other Blogs at the given website below,

https://indieseducation.com/?p=11528

You can also see a video in the given link below,

Examples : –

Q-1 The authority of advance ruling has the power of compelling the production of books of accounts . Whether the given statement is correct ?

A-1 As per section 245U authority for advance ruling has all the powers as regards code of civil procedure 1908 as refeered to in section 131 .

Authority of advance ruling (AAR) has the same power as are vested in the code of civil procedure 1908 in respect of following ,

- Discovery and inspection .

- Issuing commissions .

- Compelling the production of books of accounts and documents .

- Examine on oath.

Q- 2 Chris gayle a resident of west indies has made an application to authority for advance ruling on 02-07-2019. How ever he decided to withdraw an application on 31-08-2019. Can he withdraw an application?

A-2 As per section 245Q an applicant can withdraw an application within 30 days from the date of making an application.

Here in this case Chris Gayle has made an application on 02-07-2019 and withdrawing is application on 31-08-2019 which is after 30 days. So in this case Chris Gayle cannot withdraw his application.

Q-3 Mr. Stephen Hawking a non resident has made an appeal to authority of advance ruling. His application for the year 2014-15 is still pending in the income tax appellate tribunal. The issue was of export profit and consideration of tax thereof. The same issue was continued in 2015-16 as well.

Mr Stephen hawking’s brother Mr. Issac Newton got an approval from the authority for advance ruling for an identical issue. Mr Stephen Hawkings want to use the same rule to his case also for the year 2015-16. Can he do so?

A-3. As per section 245S (1) the advance ruling pronounced under section 245R was only applicable to a person who has sought for it and in respect of transaction in relation to which advance ruling was sought.

It shall be binding on to Principal commissioner , commissioner and an income tax authority .

In view of the above provision Mr. Stephen hawking can not use the advance ruling obtained on an identical issued by his brother Issac Newton for his assessment pertaining to the year 2015-16.

Conclusion : –

So from the above provision we can say that whenever on a particular method we don’t understand the tax structure, we can make an application to authority of advance rulings (AAR).

The solution which authority of advance ruling (AAR) suggests is to be followed by all the party engaged in the transaction as well as principal commissioner and commissioner.

FAQ’s: –

A-1 The hard copy of the application is to be filled in quadraplicate form and send to the authorized officer either by person himself or through courier or registered post with requisite fee .

A-2 AAAR stands for appellate authority of advance ruling.

A-3 An advance ruling has been obtained when a tax payer is confused about certain provisions of the act.

Advance ruling has been obtained means a ruling has been obtained before starting a particular activity.

A- 4 Scheme of advance ruling gives a platform to a non- residents for entering into joint ventures in India with other non- residents or with residents.

A-5 an applicant can enter into an advance ruling by filing GST ARA-1 and paying a fees of Rs, 5000. Once the application is recorded the said application is to be forwarded to the concerned officer for gathering the concerned records.

{kind=link}