In every business there are some assets of a fixed nature that are needed during some business activities like Building, Machinery, Plant, Furniture, Office equipment etc. that are related to depreciation.

These assets have a definite span of life after their purchase. Therefore, after their expiry, they will lose their usefulness for the business. So, fall in the value of such assets due to their constant use and expiry of time, called depreciation.

That is to say, the process of budgeting of cost of fixed assets over its life is known as depreciation.

“It refers to a gradual and permanent decrease in the value of an asset from any cause.”

Example: A machinery is purchased with the market value of rs.10,00,000 and estimated life is 10 years. In this case, cost of machinery is divided into 10 year and recorded in the books as expense i.e. 1,00,000 each year.

What you will learn:

- Importance or need of Depreciation

- Factors to consider while calculating

- Various method to calculate

- Straight line method

- Written down value method

- Methods of Recording

- Amortisation

- Conclusion

- Frequently asked questions

Importance or need of depreciation:

Here are some points to clarify that why is it necessary to calculate:

To calculate true profit or loss:

The original profit only can be ascertained if all cost incurred to earn that revenue should be debited to profit & loss A/c.

As the assets also helps in earning that revenue, this is also an expense like wages, bill etc.

For the true and fair view of financial position:

If it is not charged, the balance sheet will show that value of asset at which it is purchased which is excess of their values.

Hence, Balance sheet will not show the actual position of the business.

To know the actual cost of production:

As it is also an expense incurred in production and correct cost of production cannot be calculated unless it is also taken into account. Sale price also determined on the basis of cost of production.

However, If it is not charged, the Sale price will decrease and which will led business in reduced profits.

For avoiding over payment of tax:

If it is not calculated, the P&L A/c will show excess profit rather than actual profit. Hence, business will have to pay more tax.

To provide funds for replacement:

It is charged to P&L A/c , though it is not paid in cash like other expense.

Hence with the help of this, amount is retained in business which is further used in replacement of fixed asset after the expiry of their life span.

Factors taken into account while calculating:

Total cost of asset:

The cost of fixed asset is always determined after adding all expenses incurred for bringing that asset, such as freight and installation cost etc.

Estimated life of an asset:-

Span of life an asset is estimated in terms of year while calculating and can be used for an entity.

For example, A machine has the expected life of 10 years and its useful life will be considered as 10 years.

Estimated scrap value:

It refers to the estimated sale value of an asset after its expiry date. It is also called break up value or scrap value.

For instance, A machine has a market value of rs.1,00,000 and has span life of 5 year and at the end of which its selling value will be 8,000.

Methods of calculating :

There are various methods which are introduced for calculating depreciation,

But we will briefly discuss only first two methods as these methods are mostly used by all the business:

- Straight-line method

- Written down value method

- Annuity method

- Depreciation fund method

- Insurance policy method

- Revaluation method

- Depletion method

- Machine hour rate method

Straight line method:

It also known as the Original cost method because it charge depreciation at a fixed percentage on original cost. The amount remains fixed every year and also the method known as ‘Equal installation method’ and ‘Fixed installation method’.

In this method, devaluation are calculated by subtracting scrap value from the original market value and then divide the remaining value by no. of estimated tears of life.

Calculation :

Yearly depreciation:

Original cost of asset – scrap value of asset / Estimated life of the asset

Example– The market value of the motor car is rs.1,00,000. Hence, the scrap value is 10,000 and its estimated life is 10 years.

Calculation according to this method:

1,00,000 – 10,000 / 10 = 9,000 every year

Accounting treatment:

In case of Purchase of asset:

| Asset A/c dr |

| To bank/vendor A/c |

In case of Providing depreciation:

| Depreciation A/c dr. |

| To asset a/c |

Amount received by selling asset:

| Bank A/c dr. |

| To Asset A/c |

In case of loss in sale:

| Profit & Loss A/c dr. |

| To asset A/c |

In case of profit in sale:

| Asset a/c dr. |

| To Profit & Loss A/c |

Illustration:

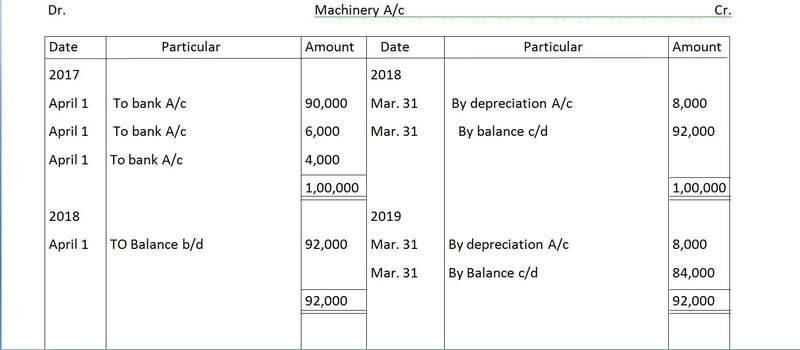

On 1st April 2019, AB ltd. Purchased a machine for rs.90,000. In addition, they spent 6,000 on its carriage and 4,000 on its erection. On the date of purchase, it was estimated that the effective life of the machine will be 10 years. Therefore, its scrap value after 10 years will be 20,000.

Solution:-

Firstly, we had to find annual depreciation:

Annual depreciation:-

= Cost of asset – Scrap Value / Estimated life of asset

=1,00,000 – 20,000 / 10 = 8,000

After that,

Rate = Amount of deprecation x 100 / Total cost of asset = 8%

Written down value method:

Under this method, as the value of asset goes on decreasing every year, the amount charged every year also goes on declining.

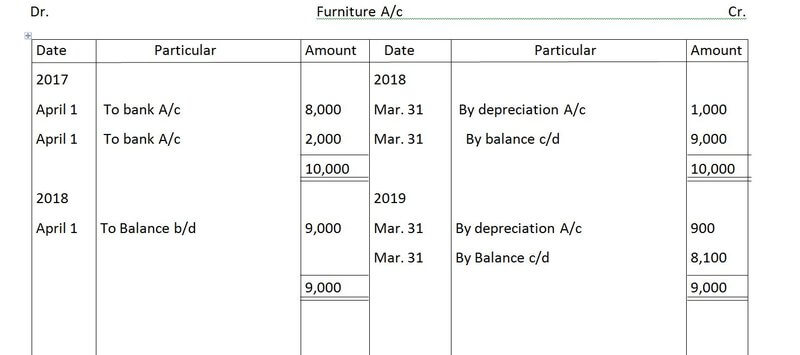

For example, furniture purchased for rs.10,000 and devaluation to be charged at 10% p.a., then it charged will be:

1st year on 10,000 i.e. @10% = 1,000 2nd year on 9,000 i.e. 10,000-9,000 @10% = 900 3rd year on 8,100 i.e. 9,000-900 @ 10% = 810

And so on,

It observed that from the above calculations that each year it is calculated on the book value of an asset rather than market value or the original value of the asset.

| Book value is the written down value of the asset. Moreover, It is that part of original cost which remains after deducting previous year depreciation. |

Book value= Original cost – Total devaluation calculated to that date

As the value of asset and amount goes on reducing every year, the method also known as ‘Reducing instalment method’ or ‘Diminishing Balance method’.

Illustration:

Majors ltd. Purchased a furniture on April 1, 2017 @ rs.8,000. In addition, they spent 2,000 on its installation. This firm charges @ 10% p.a. by written down value method and economic life is 4 years.

Methods of Recording :

By charging to asset account:

Firstly, ‘Provision for depreciation A/c’ is not maintained. Hence, the depreciation is directly charged from asset A/c. Hence, Asset A/c appears in the ledger A/c as a reduced value.

By creating Provision for depreciation A/c:

In this type of method, Amount credited to account named Provision for depreciation instead of Asset A/c.

Moreover, ‘Asset A/c’ appears in the ledger A/c at its original cost and the balance of Provision A/c is showed on the liabilities side of the balance sheet.

The accumulated amount is transferred to credit side of Asset A/c when the asset is sold, with the access of the following entry:

| Provisions for Depreciation A/c dr. |

| To Asset A/c |

Further, making the above entry, the balance in the provision account will indicate the accumulated amount on the assets in unsold assets.

Amortisation:

Amortisation is an accounting technique used to periodically lower the book value of a loan or intangible asset over a set period of time.

It is quite similar to Devaluation.

Difference between Depreciation and Amortisation:

Conclusion

Now, we learned all the basic concepts which will further help in the study. Moreover, There also one question arise that Which method is the best type of calculating? Therefore, the answer is both types are best.

Firstly, It depends on the type of firm and its types of assets etc. But, most the companies use Written down value method, It is because, this method charge the exact amount i.e. on book value.

Instead, original value method applies on the original cost which does not show the fair value of financial position because asset is consume all time and its value goes on diminishing.

Frequently asked questions

Ans: It is a mandatory deduction and the Act allows the deduction either under straight-line method or written down method. This act is 32 of the Income Tax act,

Content Marketer

{kind=link}