Meaning:-

Double taxation avoidance agreement (DTAA) means entering into a contract with another country for the prevention of chargeability of dual tax.

Giving relief from paying tax to a person who has already paid tax in some other country is a measure towards double taxation relief.

Many companies in the world are doing businesses in the other countries of the world. So they need to pay tax in the country from where they earn an income and again they have to pay tax in the country where they have their permanent establishment.This leads to double taxation of income.

For granting a relief from this, double taxation relief has been introduced by OECD ,US and UN model convention.

What’s in it for me?

- Types of relief.

- Agreement with foreign countries or specified territories (Section-90).

- Double taxation relief to be extended to agreements between specified association adopted by the central government (Section 90A).

- Taxation of business process outsourcing.

1. Types of relief: –

There are two types of relief.

- Unilateral relief.(section-91)

- Bilateral relief.(Section-90)

Now we will explain the above mentioned relief in detail,

1. Unilateral relief (section-91): –

Where there is no agreement between two countries for providing a double taxation relief at that time home country on their own provides a relief.

2. Bilateral relief (section-90): –

There are two ways of providing bilateral relief.

- Tax exemption method.

- Tax credit method.

Now we will explain the above said methods in detail.

- Tax exemption method: –

Where a company or any other person has paid a tax in any other country than by way of mutual agreement between those two countries any one country can grant a relief to that company or a person on payment of tax. This relief can be given by not paying the tax in that country.

- Tax credit method: –

Where the company has paid a tax in one country than by way of mutual agreement between those two countries other country provides tax credit relief to a company or a person for the avoidance of double taxation.

2. Section-90 Agreement with foreign countries or specified territories: –

- Central government may enter into an agreement with the government of any other countries outside India for granting of relief in respect of income on which, Tax has been paid both in India and in that other country.

- For the avoidance of double taxation of income under this act and under the correspondence of that law in force in that other country or specified territory,

- For exchange of information for the prevention of tax evasion or for the avoidance of tax,

- For recovery of income tax under this act and under that other country’s law.

- When the central government has already entered into an agreement with the other countries outside India, than the provisions of this act are applicable to assessee which are more beneficial to an assessee.

- Provisions of chapter-XA GAAR provisions are applicable to assessee even if such provisions are not beneficial to him.

- The DTAA provisions are applicable for the person who are residing in the contracting state. So this people can claim a relief on double taxation. Many a times non-resident persons also wants to take a relief on the basis of this provisions.

So for providing a relief to non-resident persons they have to submit there tax residency certificate to the government of India.

- There after the certificate issued by the government of a foreign country would constitute proof of tax residency. In relation to this if government needs any other documents or certificate than that documents or certificates are also to be provided by the non-resident to the government.

- The charge of tax in respect of a foreign company mentioned in the income tax act will be more beneficial in comparison to be mentioned in the DTAA.

3. Section 90A Double taxation relief to be extended to agreements between specified association adopted by the central government: –

Section 90A double taxation relief to be extended to agreements between specified association adopted by the central government: –

- This section specifies that any specified association of India may enter into a double taxation avoidance agreement with specified association of that other company. And central government by way of notification in the official gazette make the necessary provisions for adopting agreement for,

- Grant of double taxation relief.

- Avoidance of double taxation agreement.

- Exchange of information for the prevention of tax evasion and avoidance of income tax.

- Recovery of income tax.

- This section specifies that the provisions which are more beneficial to the assessee are applicable to non-resident person.

- Provisions of chapter X of GAAR provisions are also applicable to an assessee.

- The DTAA provisions are applicable for the person who are residing in the contracting state. So this people can claim a relief on double taxation. Many a times non-resident persons also wants to take a relief on the basis of this provisions.

So for providing a relief to non-resident persons they have to submit there tax residency certificate to the government of India.

Therefore the certificate issued by the government of a foreign country would constitute proof of tax residency.

In relation to this if government needs any other documents or certificate than that documents or certificates are also to be provided by the non-resident to the government.

Documents and information to be furnished by an assessee: –

- Status of the assessee.

- Nationality of an assessee.

- Assessee’s tax identification number.

- Period for which the tax residency certificate has been issued by the foreign government.

- Address of the assessee as mentioned in the tax residency certificate.

Countries with no agreement exists: –

In case when our country does not have an existing agreement with the another country than also relief would be granted to an assessee as per section 91 if the following conditions are fulfilled,

- Assessee should be a resident of India.

- Income accrues or arises outside India.

- Income not deemed to accrue or arise in India during previous year.

- Income in question is subject to taxable in the foreign country in the hands of an assessee.

- Assessee has paid tax in the income in foreign currency.

- And there is no agreement on relief of double taxation exists between India and that other country where the income has accrued or arisen.

In such cases assessee shall be entitled to deduction from the Indian income tax payable by him.

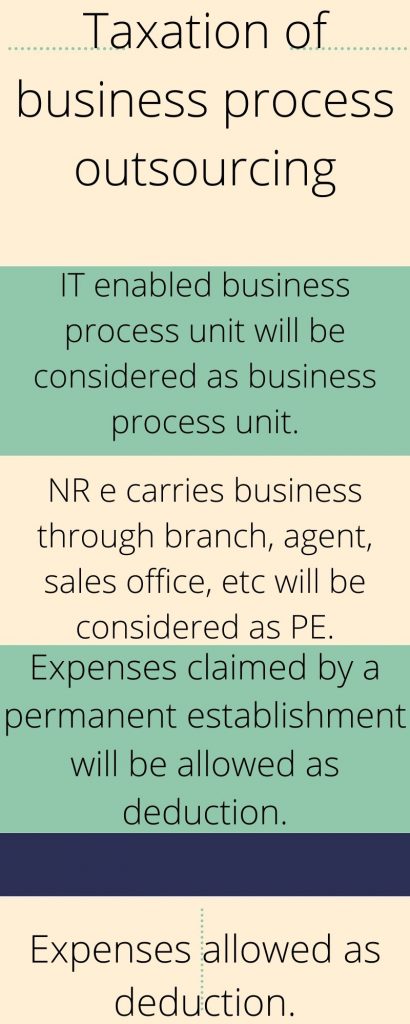

4. Taxation of business process outsourcing: –

The provisions are as under,

- Non resident may outsource certain activites to an Indian entity. If there is no business connection between the two entities than there will be no permanent establishment between the two entities. And In such a case non-resident entity will not be taxable in India.

- When non-resident entity has a business connection with an Indian business entity than there will be permanent establishment between the two entities.

- IT enabled business process unit in India will be considered as business process unit.

- Non- resident entity carries business through branch, agent, sales office, etc will be considered as permanent establishment.

- Expenses claimed by a permanent establishment will be allowed as deduction.

- All the expenses which are deductible as per income tax act,1961 are allowed as deduction.

You can also see a video on this topic at,

You can also check the above provisions in detail in the given link below,

https://www.incometaxindia.gov.in/pages/international-taxation/dtaa.aspx

You can also visit my other blocks at the given link below,

https://indieseducation.com/?p=11083

Examples: –

Shikhar Dhawan of India has earned an income in England by playing a county cricket. He has paid a tax in England on an income which he has earned from England . so if India has a double tax avoidance agreement with England , than as per section 90 he will exempted from payment of tax in India on such income.

If India does not have a double tax avoidance agreement with England, than as per section 91, India will provide relief to shikhar Dhawan.

Conclusion:-

By paying a tax in both the countries tax payer are facing hardships in the payment of tax.

To overcome this Double taxation avoidance agreement comes into place. Through this agreement taxpayer will get partial exemption or full exemption from the payment of tax.

FAQ’s: –

A-1 Double taxation avoidance agreement treaty mens a treaty which explains about the taxation procedures in case a company is earning money from two or more countries. It explains the agreements between the two countries in case double taxation occurs.

It also provides the relief provisions provided to the companies.

Through this treaty taxation of non-residents tooks place. The source country’s tax rate or the rate mentioned in the double taxation avoidance agreement , which ever is more beneficial to an assessee can be applied by that assessee.

A-2 :- currently India is having a double taxation avoidance agreement with 88 countries out of the total 198 countries in the world.

But presently with 85 countries only our double taxation avoidance agreement is in force.

Some examples are: – Unites states of America (US), United kingdom (UK), United Arab emirates (UAE), Canada , Australia , Saudi Arabia, Singapore , New Zeland, etc countries.

%20means%20entering%20into%20a%20contract%20with%20another%20country%20for%20the%20chargeability%20of%20dual%20tax.){kind=link}