{kind=link}

We all know that, In this world, all things are regulated by some predetermined rules. Accounting also runs on the fingers of golden rules of accounting.

There are some rules which are already set by some organizations of accounting.

All organisations had to maintain their accounts in accordance to that rules, because these rules are like common currency i.e. accepted worldwide.

Lets learn the official definition of accounting golden rules:

“Accounting rules refer to statements which establish guidelines on how to record transactions in the books of accounts of an organization”.

What You will get:

- Types of accounts

- Personal Account rule – 1

- Real account rule – 2

- Nominal Account rule – 3

- Illustrations

- Conclusion

- Frequently asked questions

According to the rules of accounting, all transactions are recorded on the basis of double entry system.

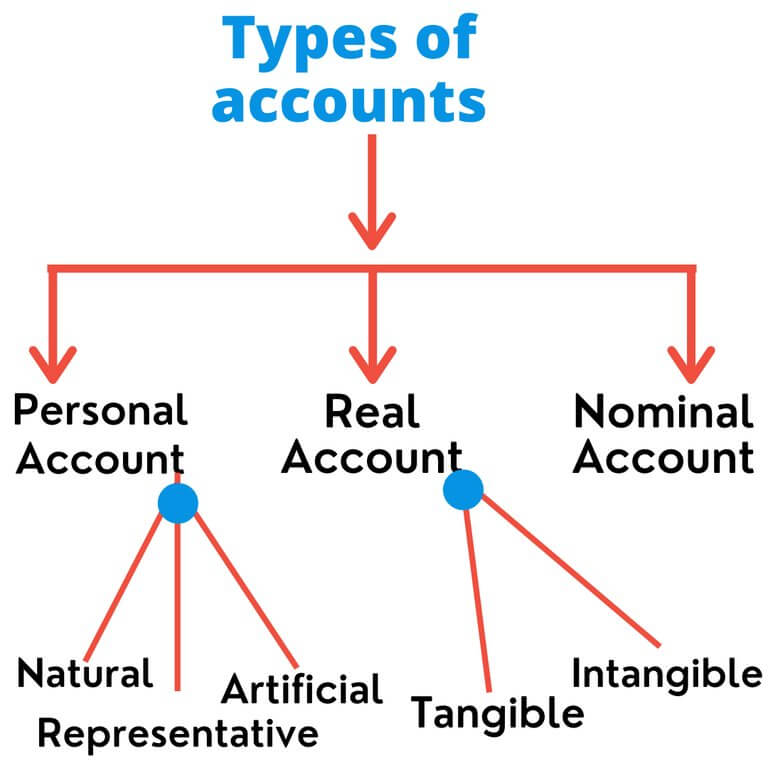

Rules of the accounting are based on the different types of accounts. So firstly we need to know about the different types of accounts.

There are three types of accounts:-

1. Personal account:-

It refers to accounts which are related to an individual, firm, company or an institution. It reflects only Personal people’s accounts.

For instance, Account of Rohan, Account of M.R.P. limited, Account of Delhi university, capital account and Drawing Account of owner.

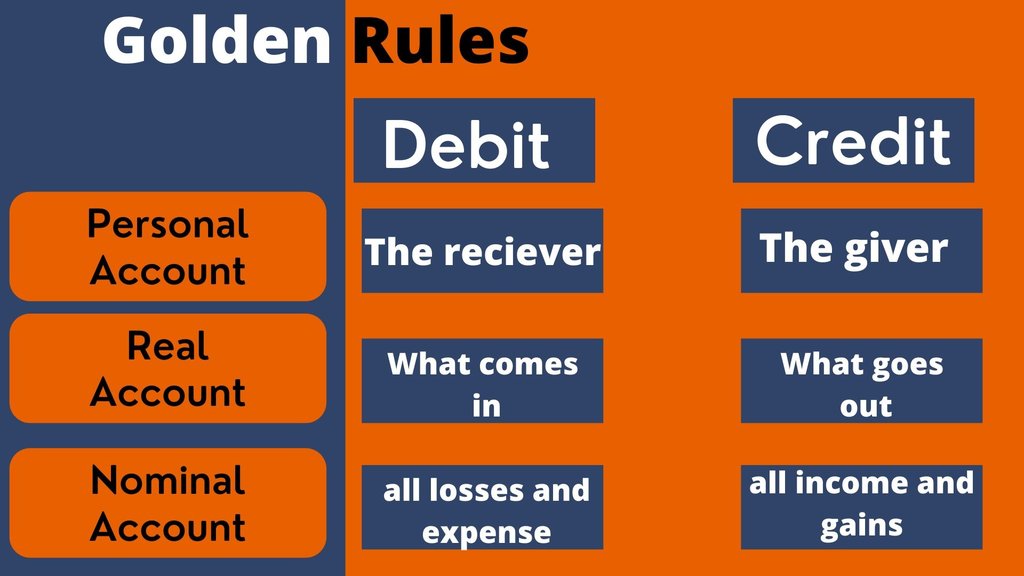

Golden Rules of Accounting – 1:-

Rules of recording in personal accounts in simple words is ‘Debit the receiver and credit the giver’.

It means that Debit that person’s account who receives something from business and credit that person who gives something to business.

Example-1:Paid rs.20,000 to Hari.

In this case, two accounts are affected i.e. Hari’s account and cash account.

According to the rule of ‘debit the receiver and credit the giver’, Hari’s a/c will be debited as he is receiver and cash a/c of business will be credited as cash has gone out.

So the entry will be:

| Hari | dr. 20,000 |

| To cash a/c | 20,000 |

Example-2: Received rs.20,000 from Hari.

In this case, two accounts are affected i.e. Hari’s account and cash account.

According to the rule of ‘debit the receiver and credit the giver’, Hari’s a/c will be credited as he pays the cash and cash a/c of business will be debited as business receives the cash.

So the entry will be:

| Cash a/c | dr. 20,000 |

| to Hari | 20,000 |

Objective:-Purpose of preparing personal a/c is to ascertain as to how much amount a personal account owes to business i.e. how much amount is due to be received and how much to be paid.

Personal account is further divided into three categories:-

| Natural Personal account | |

| Artificial Personal Account | |

| Representative personal accounts |

a. Natural personal account:-

Account of ‘Natural person’ implies the accounts of human beings.

For example, Mohan’s account, Owners’s capital account.

b. Artificial personal accounts:-

These account does not have any physical existence as human beings but they work as personal accounts.

For example, Any firm’s account, Any bank account. These are treated as artificial persons for the recording of business transaction.

c. Representative personal accounts:-

This account represents a particular person or group of members.

For instance, if the salaries for the month of January are not paid to employees, the amount payable will be added under one common title ‘salaries outstanding account’.

Real accounts:-

It refers to the account of all such things whose value can be measured in money and which can be the properties of business.

Such as cash a/c, furniture a/c, machinery a/c etc.

Golden rules of Accounting- 2

Rules for recording the transaction in the real account is ‘Debit what comes in and credit what goes out’.

According to this, Whenever any property comes in the business is debited and when it goes out, it is credited.

Example: A machinery purchased for rs.20,000 for cash.

Machinery a/c should be debited according to rule ‘debit what comes in’ and cash a/c is credited because cash is gone out.

Therefore, the entry will be:

| Machinery a/c | dr. 20,000 |

| To cash a/c | 20,000 |

Objective:-These accounts shows the value of various properties which are owned by business and represents the financial position of business.

Types of real accounts:-

| Tangible real accounts | |

| Intangible real accounts |

a. Tangible real accounts:

It refers to the account of those things which can be touched, felt, measured, etc.

Stock a/c, furniture a/c and cash a/c are some examples.

b. Intangible real accounts:

These accounts represents such thing cannot be touched but can be measured in terms of money.

For example, goodwill a/c and patent a/c etc.

Nominal accounts:

Nominal accounts include accounts which are related to all expenses and incomes.

For example, Accounts related to expenses are: salaries paid, discount allowed etc. Accounts related to incomes are: commission received, discount received etc.

Golden Rules of Accounting- 3

The rule for recording in this account is ‘debit all losses and expense and credit all income and gains’.

Example-1:- Paid rs.20,000 salaries.

In this case, two accounts are affected i.e. salaries a/c and cash a/c.

Salaries a/c show expenses and it is debited according to the rule. On the other hand, cash a/c is credited as it shows about the income.

So the entry will be:

| Salaries a/c | dr. 20,000 |

| To cash a/c | 20,000 |

Example-2:- Received rs.5,000 for commission.

In this case this two accounts i.e. commission a/c and cash a/c are affected.

Commission a/c is nominal a/c and shows about the income, so it will be credited and Cash a/c is a real a/c which will be debited according to rule ‘ debit the expenses’.

So Entry will be:

| Cash a/c | dr. 5,000 |

| To commission a/c | 5,000 |

Objective:-These are the accounts that are in name only and which do not already exist.

These are opened simply to explain the nature of head for which cash has been paid off.

In the absence of nominal accounts, it will be very difficult to manage all expenses and incomes of an business.

| Types of accounts | Golden Rules |

|---|---|

| Personal Account | Dr. – The receiver Cr.- The giver |

| Real account | Dr.- what comes in Cr.- what goes out |

| Nominal account | Dr.- all expenses and losses Cr.- all income and gains |

Some Illustrations and examples:

Classify the following account into personal, real and nominal accounts:

| 1.Capital | 9. Furniture | 17. Patents |

| 2. Drawing | 10. Cash a/c | 18. Salary a/c |

| 3. Cash paid | 11. Bank a/c | 19. Salary outstanding a/c |

| 4. Cash received | 12. Bank overdraft a/c | 20. Insurance a/c |

| 5. Commission paid | 13. Debtors a/c | 21. Insurance prepaid a/c |

| 6.commission received | 14. Creditors a/c | 22. Bad debts written off |

| 7. Purchase a/c | 15. Traveling expenses | 23. Bad debts recovered |

| 8. Sales a/c | 16. Goodwill |

Solution:-

| Personal A/c | Real A/c | Nominal A/c |

|---|---|---|

| 1. Capital | 3. Cash paid | 5. Commission Paid |

| 2. Drawings | 4. Cash received | 6. Commission received |

| 11. Bank A/c | 9. Furniture A/c | 7. Purchase A/c |

| 12.Bank overdraft A/c | 10. Cash A/c | 8. Sales A/c |

| 13. Creditors A/c | 16. Goodwill A/c | 15.Travelling Expense A/c |

| 14. Debtors A/c | 17. Patents A/c | 18.Salary A/c |

| 19. Salary Outstanding A/c* | 20.Insurance A/c | |

| 21. Insurance Prepaid A/c* | 22.Bad debts written off | |

| 23. Bad debts Recovered |

Notes:

(i). Salary A/c is a nominal A/c but Salary outstanding A/c is a Personal account because it is the account of some unnamed creditor.

(ii). Insurance A/c is a nominal A/c whereas Insurance prepaid A/c is a personal A/c because it is an account of some unnamed debtor.

Conclusion:-

As we learn that all accounts are prepared on the basis of golden rules of accounting in a very systematic manner.

But what would happen, if there are no any rules. Without the commencement of rule, all business would record their transactions in their own way and it may create various confusions among various industries.

For example, A ltd. Records their transaction in such a way that dr. all incomes and cr. all expenses.

On the other hand B ltd. Records as dr. all expenses and cr. all incomes.

Now they records their transaction in a opposite way. So it makes difficult for some common users like investors, public, banks, and also their owners.

They would become confused regarding incomes and expense that directly affect asset and liabilities of that business.

This can present wrong financial position of that company and the users would not take the proper decisions regarding the company.

This would lead loss to both i.e. users and company. So it is very essential to follow common rules established by financial institutions.

Frequently asked questions

Ans: The double entry system of accounting was formally written in a book by an Italian mathematician Fra Luca Pacioli and his close friend Leonardo da Vinci and the golden rules are considered as part of this.

Content Marketer