Goods and services tax is an indirect tax charged at a prescribed rate on every supply of goods and services consumed for domestic purposes.

It is a nation-wide tax and adopted to merge various indirect tax such as Service tax, excise duty, etc.

Goods and services tax is based on the principle of ‘one nation one Tax’. It was implemented in India to remove the policy of double taxation.

It is transferable tax i.e. can be transferred from one person to another.

For example, A buyer purchased chips from the seller and paid price and GST to the seller. In this case, the seller transfers his tax to the buyer.

GST is always paid by the end-user of that product or final consumer of that product. GST is paid by consumers but remitted to the government with the help of business.

What’s in it for me:

- Taxes merged into GST

- History of GST

- Slabs or structure of GST

- Goods and services excluded from GST

- Types of taxes

- Accounting treatment

- How to calculate GST

- Conclusion

- Frequently asked questions

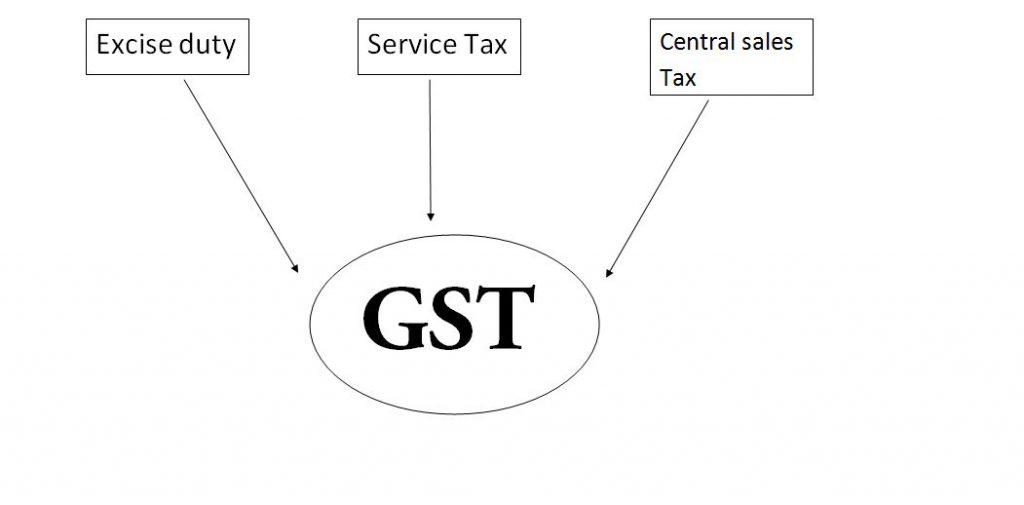

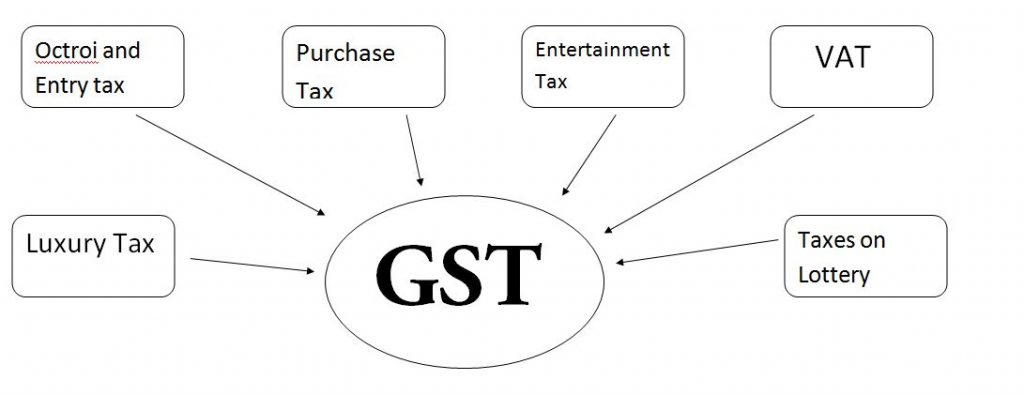

Taxes Merged into Goods and Services tax:

GST has replaced many indirect taxes imposed by Central and State Governments.

Central level taxes that have merged into GST:

State level taxes that have merged into GST:

History of GST:

France was the first country to adopt the Goods and Services tax in 1954. Then the estimation was 160 countries also implemented the same tax in their country.

In India, After GST council approved the CGST Bill 2017, IGST Bill 2017, UTGST Bill 2017, GST Bill 2017 (Compensation of all bills), Lok Sabha passed bills on 29th March 2017 and on 6th April 2017 Rajya sabha approved the bill and approve as a bill on 12th April.

After that, the state legislature of different states has passed that bill. After the approval of the bill, It came into force on 1st July, 2017.

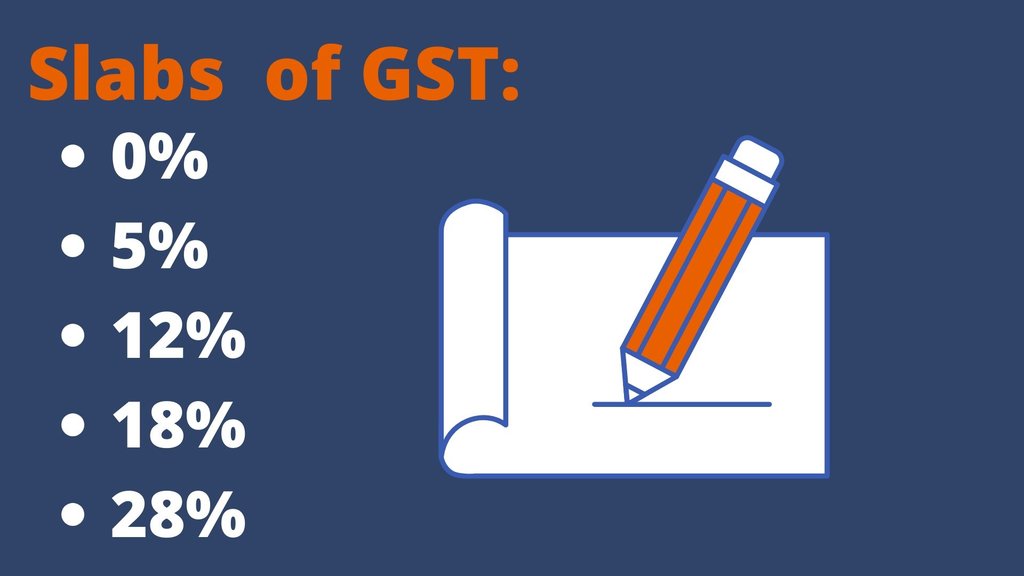

Slabs or structure of GST:

Goods and services are divided into 5 categories for the collection of tax :

0% Tax slab rate

7% of the goods and services falls in this category. This category includes essential items for survival.

For example,

| Fresh fruits | Honey | Cereals |

| Vegetables | Butter | Meat |

| Milk | Flour | Eggs |

| Curd | Besan | coloring books |

| Stamps | Printed books | Hotels |

| Judicial papers | Newspapers | Tariff plans under rs.1,000 |

5% slab rate

14% of all goods and services are counted in this slab. It consists of the items which have common use in our life.

For example,

| Clothes | cream | milk powder |

| footwear | frozen vegetables | coffee |

| Packaged food | spices | tea |

| pizza bread | rusk | ice |

| fish fillet | kerosene | coal |

| medicine | incense sticks | small restaurants |

12% slab rate

This slab also called the standard rate of GST. 17% of goods and services are fall under this category.

For example,

| frozen meat | cheese | ghee |

| butter | dry fruits | animal products |

| namkeen | sauces | cellphones |

| kitchen utensils | carom board | Chess |

18% slab rate

It includes It services, restaurants, camera, electronic gadgets, monitor, speakers, all steel products, aluminum foil, telecom services, branded footwear and clothes, mineral water, preserved vegetables, jams, soups, ice cream and so on.

This rate includes 43% of all goods and services of all products.

28% slab rate

It includes all luxury items and items which are injuries to health like tobacco, wine, cigarettes, etc.

| Shampoo | Shaving creams | Sunscreen |

| Paint | Dishwasher | Weighing machine |

| Water heater | Vacuum cleaner | Automobiles |

| Private lottery | Chewing gum | Motorcycles |

| Luxury cars like Audi, BMW |

Important Notes:

* Sellers purchase goods and pay GST for the purpose of reselling, they consider GST as their asset not as a cost or expense, because they had to recover that amount from the buyers of that product.

*Sometimes, In certain cases, GST paid cannot set off against GST collected. In such cases, GST paid considered as a cost for the purchaser.

This situation happens in the following cases:

- Payment for health insurance.

- Free gift to staff.

- Purchase of vehicles.

- Payment for goods and services for personal use.

- Repairs and maintenance of buildings and other assets.

Sometimes GST is reversed in following cases;

- Purchase returns.

- Goods lost or stolen.

- Destroyed or become non-saleable.

- Goods are given away as charity.

- Distributed as free samples.

Some Goods and Services are Excluded from Levy of GST:

- Payment of wages and salaries.

- Petroleum.

- Electricity and water bills.

- Interest.

- Educational services…. And so no.

Types of Taxes considered under GST:

Central GST (CGST):

These taxes are imposed on intra-state sales i.e. within the same state under the CGST act. The central government collects this tax.

For example, Rajesh from Haryana sells goods worth 10,000 to Mahesh from Haryana and the tax rate is 18% and Ramesh collects 1,800 as GST and pays 900 to the Centre government. These taxes are divided into central government and state governments.

State GST (SGST):

These are also like the CGST as levied on intra-state transactions or within the same state under the SGST act and collected by State government.

For example, In the above example, Rajesh paid 900 to the central government and now remained 900 will paid to the state government.

Integrated GST (IGST):

This tax is applied to inter-state sales i.e. sale of goods and services from one state to another state. It is also levied on the import of goods and services into India as well as export from India.

For example, A dealer from Gujrat sells goods worth 50,000 to a dealer in Madhya Pradesh. Suppose, the IGST rate is 12%. In this Seller charge, 6,000 as IGST and the whole amount are paid to the central government.

GST collected under IGST is divided into both Central and state governments as per the rates decided by the government.

Accounting Treatments:

In case of intra-state sales of goods and services ( within same state)

For purchase of Goods:

| Purchases A/c Dr. Input CGST A/c Dr. Input SGST A/c Dr. |

| To Bank/Creditors A/c |

For sale of Goods:

| Bank/Debtors A/c Dr. |

| To sales A/c To output CGST & SGST A/c |

Ssetting off Input CGST against Output CGST:

| Output CGST A/c Dr. |

| To Input CGST A/c |

For setting off Input SGST against Output SGST:

| Output SGST A/c Dr. |

| To Input SGST A/c |

For Payment of remaining GST:

| Output CGST A/c Dr. Input SGST A/c Dr. |

| To Bank A/c |

In case of interstate sale of goods and services ( to another state):

Purchase of goods:

| Purchases A/c Dr. Input IGST A/c Dr. |

| To Bank/Creditors A/c |

Sale of goods:

| Debtors/Bank A/c Dr. |

| To sales A/c To output Igst A/c |

Adjustment of IGST:

| Output Igst A/c Dr. |

| To Input IGST A/c |

How to calculate GST:

Total amount of GST:

If you want to calculate the GST amount to be charged on selling price or to add GST into that amount. All you need to do is to first find the percentage amount to be charged on price and then add it to the selling price.

For example, The selling price is 20,000 and the rate of GST is 12 %, So firstly find the amount of percentage and then add it to selling price i.e. 20,000. So the %tage amount is:

20,000 x 12/100= 2,400 ( GST amount) 20,000 + 2,400= 22,400 (Total amount)

Total amount including GST:

If you want to find the original amount of GST charge and to find the GST inclusive amount then simply take a percentage and add 1 to it, then multiply it by the original amount.

For example, The selling price is 20,000, and the GST rate is 12%. Then add 1 to 12% and then multiply it by 20,000

= 12% + 1 = 12/100 + 1 = 0.12 + 1 = 1.12 Now, 20,000 x 1.12 = 22,400 ( total amount including GST)

GST amount from Selling price:

Sometimes the total amount is given which includes GST amount and selling price and you want to find out the GST amount. Then firstly add 1 to the GST percentage and divide it to total amount including GST price and then subtract that amount from the given amount.

For example, The Total amount including GST is 22,400 and the rate of GST is 12%, then,

12% + 1 0.12 + 1 = 1.12 Now, 22,400/ 1.12 = 20,000 22,400-20,000 = 2,400 ( Amount of GST charged )

Conclusion

At last, we can conclude that the implementation of GST in India gave some relief to Business as well as the Government.

Before the GST, there are a lot of taxes charged on sale and purchase transactions and make the whole process confusing.

Sometimes, Businesses had to pay one tax double time due to the policies of taxes and reduce their profit margin, but now, with the introduction of tax named ‘one nation one tax’ the whole process becomes simple and now can calculate tax very easily.

Frequently asked questions

Ans: It is not necessary but suggested to hire a CA firm to file the GST returns. A normal person is ought to face technical difficulties if he/she has no idea about how to go about it. So if you lack deep insight into the GST act and rules, you should hire a CA to file returns and understand the nuances.

Ans: India adopted a dual GST model, meaning that taxation is administered by both the Union and state governments. Transactions made within a single state are levied with Central GST (CGST) by the Central Government and State GST (SGST) by the State governments.

Ans: The excess GST paid can be claimed as a refund within two years from the date of payment. This means that if excess GST is paid in the month of November 2017, GST refund application can be submitted until November 2019

Content Marketer

{kind=link}