Any registered taxpayer under the GST regime can apply for GST cancellation under certain conditions as described by the GST department, in case he/she wants to close his registration.

Now we are going to have a look into what is GST cancellation and how to cancel GST registration in case you need it.

Table of Content

- What Is GST Cancellation?

- Voluntary GST Cancellation

- Procedure For GST Cancellation

- Cancellation By The Tax Officer

- Revocation Of Cancelled GST

- Frequently Asked Questions

What Is GST Cancellation?

GST registration cancellation simply means that a registered person is no longer in need of the GST number, so he/she wants to cancel his/her registration.

Sometimes, the registration can also be cancelled by the government due to not maintaining the regulatory compliances under GST or conducting business against the GST guidelines.

The taxpayer is not responsible for paying or collecting tax from anyone after the cancellation is successfully done. The person also cannot conduct any business for which GST registration is mandatory.

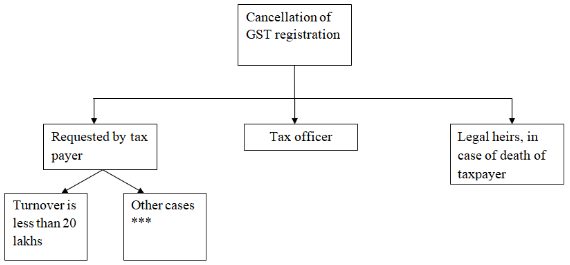

Any one of the following can be there for cancellation of GST registration.

- Voluntarily cancellation by the registered taxpayer

- Cancellation by the tax officer

- By the government due to non-filing of GST Returns

- By legal heirs, in case of death of the registered taxpayer

Voluntarily GST Cancellation

As per the guidelines under Section 29 of the CGST Act, voluntary cancellation of GST can be made by any registered person only under the following conditions –

- The registered person is no longer continuing the business for which he has taken the registration of GST.

- The business for which the GST was taken is merged, demerged, or transferred into some other company. In this case, the new business has to apply for a new registration after the cancellation and closure of the earlier business.

- There is a change in the nature of the business, for example, proprietor to private limited, etc.

- Turnover of the registered person becomes less than the threshold limit as described under the GST regime.

- If the proprietor of the business has passed away, in this case, the legal heir of the taxpayer can apply for cancellation.

If you want to cancel GST registration voluntarily, then you must ensure that all the GST returns must be filed up to date.

In case you have haven’t filed the returns of the previous months, then any due penalties have to be paid before applying for cancellation.

Procedure For GST Cancellation

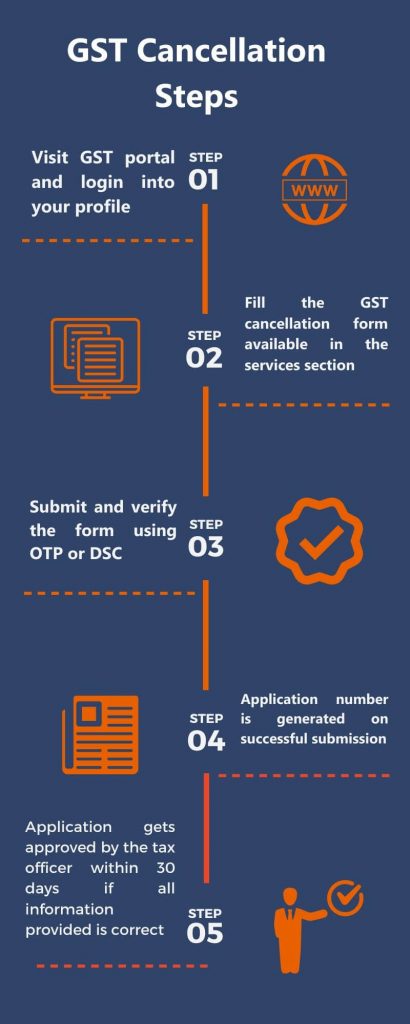

A registered taxpayer can apply for cancellation on the common good and service tax portal. Let us now see how to cancel GST number by following the given steps –

- The person has to make an application request on the GST portal known as FORM GST REG-16. The form is available in the services section on the GST portal.

- All the details in the form need to be filled then the verification is to be done using OTP or DSC for submission of the form.

- The application number is then generated after successful submission of the form.

Once you submit the application, the concerned tax officer will evaluate the application and will approve the request within 30 days, if all the cancellation criteria is met.

The tax officer will then issue an order of cancellation mentioning the exact date of cancellation.

Cancellation By The Tax Officer

The tax officer has the authority to cancel the GST of a registered taxpayer as a result of any violation of rules as defined under the GST regulations.

Below are the factors on which the tax officer can cancel the GST –

- No business is being conducted from the registered place of business.

- Business is started but the signboard is not displayed at the registered place of business.

- Additional business is done from the place but it is not declared in the GST portal.

- The taxpayer has not filed the GST returns for an extended period of time.

- Illegal or unethical activities are being conducted from the registered place of business.

- The taxpayer has issued invoices but has not supplied any goods or services.

- The taxpayer has supplied any goods or services but not issued any invoice against it.

The tax officer sends a notice for cancellation to the registered taxpayer if any of the above-stated reason is found.

Therefore, the taxpayer has to reply to the notice within seven days of issuance of the notice, explaining why his registration should not be cancelled.

The tax officer with drop the cancellation process only if the reply is found to be satisfactory by him.

If the reply is not satisfactory then tax officer will issue an order of cancellation in FORM REG-19 within 30 days from the date of reply to the notice.

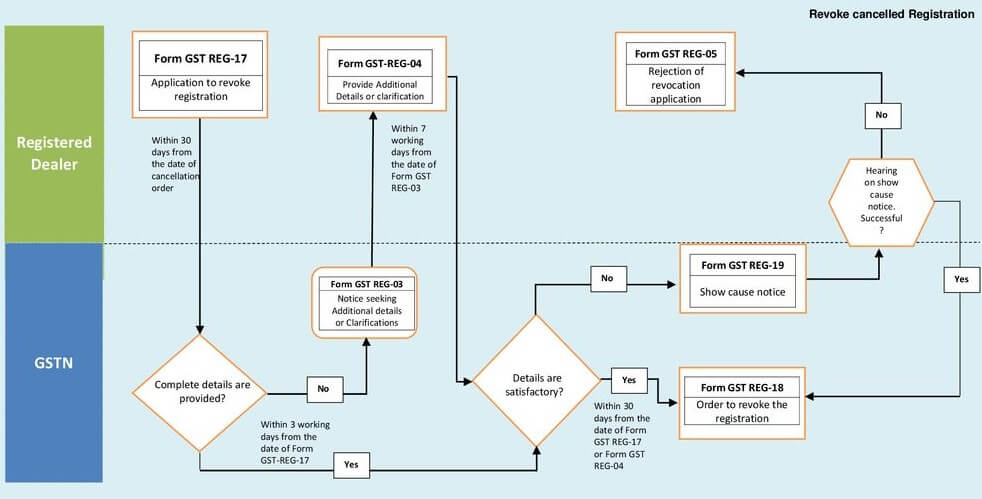

Revocation Of Cancelled GST

GST revocation means to reverse the order of cancellation of GST. In other words, it means to activate the registration number again.

The revocation can only be done in case the GST is cancelled by the tax officer. It cannot be done if the cancellation is due to the non-filing of returns.

The registered taxpayer firstly has to submit an application from the GST portal for revocation of cancelled GST.

The application has to be done within 30 days of receiving the order of cancellation from the tax officer.

If the tax officer is satisfied with the revocation application then he will reverse the cancellation order within 30 days by giving an order, and the registration will become active again.

If the tax officer is not satisfied with the revocation application, then he can either reject the application or can give a chance to the taxpayer to explain why his application should not be rejected by issuing a notice.

Therefore the taxpayer has to reply to the notice within seven days of issuance of such notice. The tax officer will then take the final decision within 30 days to accept or reject the reply given by the taxpayer.

Frequently Asked Questions

Now let us discuss some frequently asked questions on GST Cancellation.

GST cancellation status can be checked on the GST website in the Track Application Status option, by mentioning your ARN (application) number.

GST cancellation certificate can be downloaded from the GST website in the view/download certificate option.

A cancelled GST can only be activated if it is cancelled by the tax officer. The application for revocation has to be done within 30 days of the order of cancellation.

The taxpayer has to file a final return within three months of the cancellation of the GST number. This return ensures that the taxpayer does not have any outstanding liabilities against the cancelled GST.

The taxpayer cannot apply for the cancellation of GST until he has filed all the returns up to date.

Generally, it takes 30 days from the date of application to get the GST number cancelled.

GST can be cancelled by the respective tax authority in the following conditions-

1. Not filing GST Returns for six months continuously

2. Not paying taxes

3. Violating any of the regulations as described under the GST regime

4. No business conducted for the last six months after taking GST registration

There is no fee for the application of the cancellation of GST but if you take the help of any consultant for cancellation, then he/she will charge you their professional fee.

The GST number is suspended once the application is filed for cancellation. So it is not mandatory to file the GST NIL return. Although it is advisable to file the NIL returns till the time the application is approved the tax officer.

Any person or company registered as Tax Collector or Tax Deductor or is allotted UIN (Unique Identification Number), cannot apply for GST cancellation.

Yes, a person can file all the pending returns even if the GST number is cancelled by the tax officer.

The maximum penalty for GST is fixed by the government at Rs.5,000.

Yes, there is a penalty of Rs.200 per day or maximum Rs.10,000, if the final return is not filed before three months of the date of cancellation of GST.

1. Form GST REG 16 – Cancellation form by a registered person

2. Form GST REG 17 – Issue of show cause notice for cancellation by the tax officer or tax authority

3. Form GST REG 18 – Reply to the show cause notice by the registered person

4. Form GST REG 19 Order for dissolution

5. Form GST REG 20 – Form to stop the ongoing cancellation proceedings

6. Form GST REG 21 – Application to revoke the cancelled GST

7. Form GST REG 22 – Order revoking the cancellation of GST

E Way Bill also gets blocked once the GST is cancelled either by the government or on a voluntary basis.

{kind=link}