Meaning of Non-resident taxation:-

A person who is not a resident of India but is required to pay tax on certain income which he has earned from India is covered under non-resident taxation.

Mr. Steve smith a cricketer of Australia has came to India for playing an IPL. So an income which he earns by playing an IPL should be taxable in India?

Well the answer is Yes!!!!!

He is covered under the provisions of non-resident taxation.

Let us understand this topic in detail.

What’s in it for me?

1. Residential taxation of total income of a Non-resident :-

Section-6:- Residential status of a non-resident person:-

- Resident and ordinary resident (ROR).

- Resident and not ordinary resident (RNOR).

- Non-resident (NOR).

Residential status of an individual:-

Basic conditions,

In the previous year a person should be remain in India for >/182 days.

OR

A person should be remain in India for total period of 365 days in previous 4 years

AND

in the previous year also he should be remain in India for at least 60 days.

Exceptions to above conditions:-

(Only first condition will apply).

(Second condition will not apply).

- A person remains outside india in the previous year as a member of crew or for the purpose of employment outside india.

- An Indian origin person comes to a visit to india during the previous year.

Additional conditions:-

- In the previous 7 years he should be remain present in India for at least 730 days or more.

AND

- He must be resident in India for at least 2 years out of the last 10 years.

- If person fulfills any 1 basic condition and 2 additional conditions than he will be termed as resident and ordinary resident (ROR).

- If person fulfills any 1 Basic condition and any 1 additional condition than he will be termed as resident but not ordinary resident. (RNOR)

- If person does not fulfill any basic condition than he will be termed as Non-resident.

Residential status of an HUF/AOP/BOI/Local authorities and Artificial jurisdiction person:-

Resident:- This person would be considered as a resident of india , if their control and management of affairs is situated in india.

Non-resident:- If their control and management is situated wholly outside india they will considered as Non-resident.

Control and management of HUF:- It is with Karta or its Manager.

Control and management of AOP and BOI:- it is eith Partners and Managers.

Residential Status of HUF:-

If karta of HUF satisfies both the additional conditions than HUF status will be considered as Resident and Ordinary Resident.(ROR)

If Karta of HUF does not satisfy does not satisfy the additional conditions than it will be treated as resident but not resident. (R NOR)

Residential status of a company:-

A company will be considered as an Indian company if,

- It is incorporated in india.

- Its Place of effective management(POEM) is in india.

Principles for determination of POEM of a company other than an Indian company:-

A company shall be said to be actively engaged outside india if the following conditions are satisfied,

- If passive income is <50%.

- If <50% of employees are situated in india.

- If <50% of assets are situated in india.

- If <50% of payroll expense of employees are incurred in india.

On satisfaction of all the above conditions we can say that the company is said to be actively engaged outside India.

Meaning of passive income:-

- Income from transactions both purchases and sales is from and too an associated enterprise.

- Income from Interest, Royalty, Capital Gains, Rental income or dividend whether or not involving associated enterprises.

For more information on Resident Taxation visit a website of Ministry of Finance given below.

https://finmin.nic.in/sites/default/files/NonResTax.pdf

2. Scope of total income of a Non-resident (section-5):-

The scope of total income of an assessee depends upon the following three conditions:-

- Residential status of an assessee.

- The place of accrual or receipt of income whether actual or deemed and,

- Point of time at which the income has accrued or was received on behalf of an assessee.

Non-Residents total income should includes,

- Income received or deemed to be received in india in the previous year and,

- Income which accrues or arise or deemed to accrue or arise in india in the preceding previous year.

Income deemed to be received in India:-

- Contribution received in recognized provident fund is in excess of 12% or interest credired in excess of 9.5%.

- Contribution by Central government or other employer under a pension scheme u/s80CCD

- Amount transferred from unrecognized provident fund to recognized provident fund.

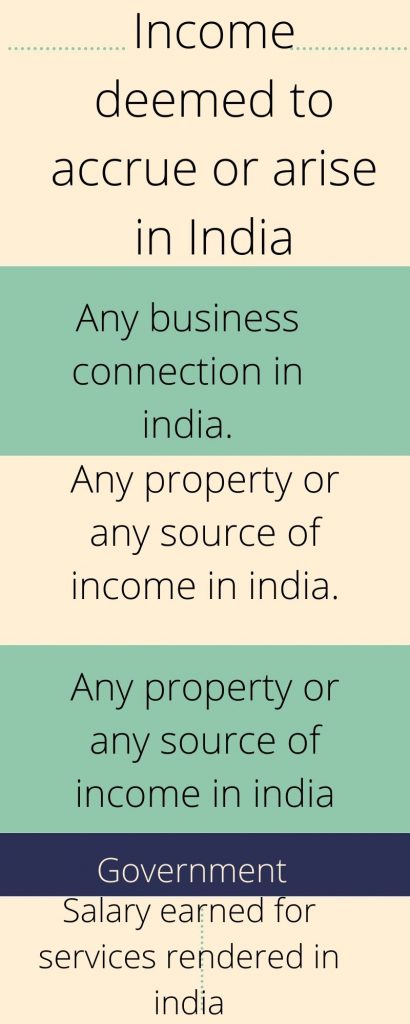

Income deemed to accrue or arise in India:-

- Income accruing or arising outside india directly or indirectly through or from,

- Any business connection in india.

- Any property or any source of income in india.

- Transfer of capital asset situated in india.

- Salary earned for services rendered in India.

- Salary payable by government to Indian citizen for services rendered outside India.

- Dividend paid by Indian company outside India.

- Interest, Royalty or Fees for technical services payable by,

- Person resident in India.

- Government.

- A non-resident.

(Non-resident :- If money has borrowed by a non-resident for the purpose of business or profession carried on in India).

Non-resident in the following cases shall not be treated as business connection in India: –

- Business in respect of which all the operations are not carried out in India.

- Purchase of goods in India for export.

- Collection of news and views in India for transmission out of India.

- Shooting of cinematographic films in India.

- Activites confined to display of rough diamonds in SNZ’s.

Exempt income of non-residents:-

- Interest on money standing to the credit in non-resident external account. Sec10(4)(2)

- Interest on saving certificate issued by the central government. Sec10(4B)

- Remuneration received by foreign diplomats. Sec10(6)(2)

- Services rendered on foreign ships and total stay in india is less than 90 days. Sec10(6)(8)

- Remuneration received as an employee of the government of a foreign state during his state in india in connection with his training in any government office,etc. sec(10)(9)

- Tax paid by government or indian concern on income derived by way of royalty or fees of technical services by the foreign company from government or Indian concern. Sec(10)(6A)

- Income arising by way of royalty from fees or technical services rendered in or outside india to, the national technical research organization(NTRO). Sec(10)(6D)

- Foreign income. Sec(10)(9)

- Interest on deposits made by foreign bank with schedule bank with approval of RBI. Sec(10)(15)

- Interest on deposits in offshore banking unit. Sec(10)(15)

- Income of SAARC fund for regional projects set up by colmbo declaration. Sec10(23BBC)

- Income received in india in Indian currency on account of sale of crude oil or any other goods or rendering of services as may be notified by the central government. Sec10(48A)

- Income accruing or arising on account of storage of crude oil in a facility in india and sale of crude oil therefrom to any person resident in india. Sec10(48A)

- Income from sale of leftover stock of crude oil fromfacility in india after the expiry of agreement as may be notified by the central government. Sec 10(48B).

If you want to see a video on this you can visit this channel,

You can also visit my other blogs at,

https://indieseducation.com/?p=9069

Examples: –

Resident and ordinary individual:-

Example-1

Q-1 MR gotiwala in the previous year remains in India for 180 days but in the last 4 previous year he remains in India for 900 days. Whether he should be considered as resident and ordinary resident?

A-1 As in the last 4 years he remains in India for more than 360 days he will be considered as resident in India. ( He fulfills 1 basic conditions.)

In the last 7 years he remains in india for more than 730 days as well as he also remains in india for 2 preceding previous year from the last 10 years. As both the additional conditions are satisfied he will be said as resident and ordinary resident in india.

Example-2

- Mr Justin Biber of USA has visited India for the collection of news. Whether his visit in India will be considered as business connection in India?

- No. His visit is specifically excluded from the definition of business connection.

Conclusion:-

Non-resident taxation provisions are applicable to all the non-residents for the determination of tax liablity in India.

FAQ’s:-

Q-1 On how much amount non-residents will pay the tax?

A-1 income which is earned from India or is deemed to accrue or arise in India is only taxable in the hands of the non-residents.

A-2. No. If TDS has been deducted on the income payable to non-residents than again non-resident is not required to pay tax.

A-3 Yes. Non-residents are required to pay GST as per the GST act. If their income increases certain limit than they have to pay GST.

A-4 No. They are not compulsorily required to take GST. If they voluntary want to take registration than they can take a registration.

A-5 It includes ,

· Transfer of all or any rights relating to Patent invention, model, design, secret formula, process, trademark or similar process.

· Imparting of any information or any use of patent invention, model, design, secret formula, process, trademark or similar process.

· Use of any patent, model, design, secret formula, trademark or similar process.

· Imparting of any information concerning technical, industrial, commercial or technical , scientific knowledge, experience ,skill.

· Use of right to use of any information concerning technical, industrial or technical skill.

· Transfer of all or any rights in respect of copyright, literary, artistic or scientific work.

· Rendering of any service in connection of any activites listed above.

{kind=link}