After ascertaining the true net profit or loss by Preparing the Trading, Profit & Loss A/C of the business, The owner would also curious to know the exact financial position of Business i.e. about their asset and liabilities. (Balance sheet)

For this purpose, Enterprise prepares a statement which tells us about the asset and liabilities of the Business, called Balance sheet.

It is termed as a sheet because it shows the balances of ledger accounts that are still open and have some balance whether it is debit or credit.

“Balance sheet refers to a statement prepared with a view to measure the exact Financial Position of a Business on a certain fixed date.”

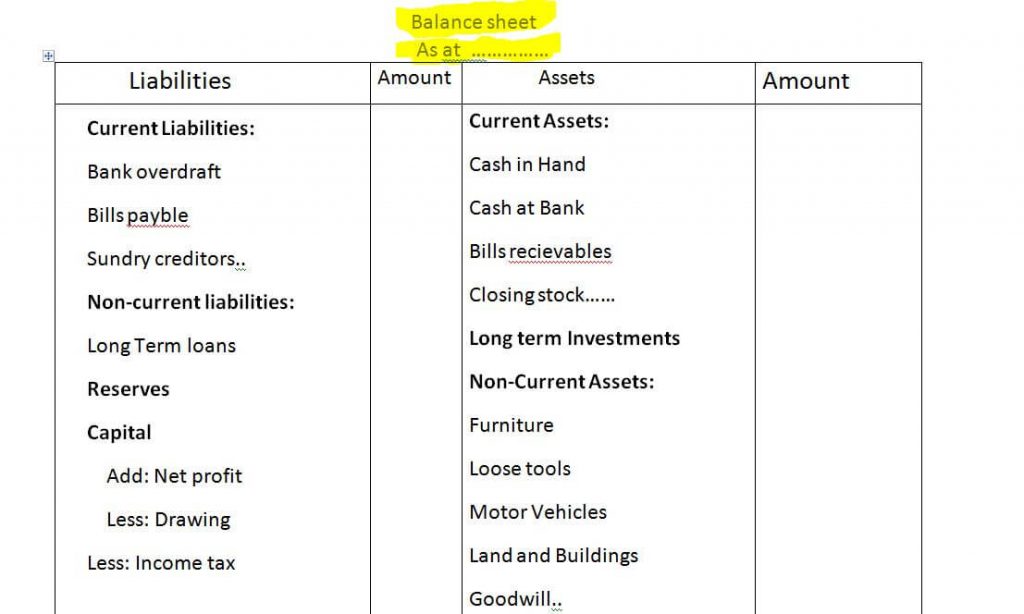

This sheet consists of two sides i.e. Asset and Liabilities. The left-hand side contains all the Liabilities and the capital of proprietor and all Assets written on the right side of the Balance sheet.

| Assets = Liabilities + Capital |

What you will get:

- Features

- Importance

- Grouping of Assets and Liabilities

- Marshaling of assets and Liabilities

- Classification of Assets

- Classification of Liabilities

- Conclusion

Format of Balance sheet

Some key features:

Part:

It is a part of financial accounts. That’s why, final accounts consider the Trading, Profit & Loss A/c and Balance sheets together.

Statement:

It is a statement not an account so that It doesn’t have any debit or credit side, and the words like ‘by’ or ‘to’ not used before the terms.

Summary:

This is the summary of such Personal and Real account which are still open and have not been closed by transfer into Trading, Profit and Loss A/c.

Format:

Debit balances of accounts transferred on the right side (Asset side) and credit balances put on the left side called the Liabilities side.

Total:

The total of both must be equal, if there are not equal, there will be an error which is happened somewhere.

Preaparation:

Firm prepares the Balance sheet on a particular date not for a particular period. As it shows the financial position of an entity on a particular date.

For example, A firm prepares their accounts on 31st March 2019, It means that it shows only the assets and liabilities which they have on 31st march. If there will any transaction happened, it causes all changes in the Balance sheet.

It is prepared on the principle of ‘going concern concept’.

Need and Importance of Preparing:

As we know that If a Business does not know what do they have and from whom they owe, they cannot survive in the long term. So, Here is some key Importance which we need to know:

1. The main purpose is to ascertain the true financial position of the business at a particular date.

2. It helps in ascertaining the nature and balance of various assets like Closing stock etc. and also the amount of several liabilities.

3. It gives information about the exact amount of capital at the end of each year. It shows the addition and deduction in the capital like drawings etc.

4. It helps in finding out whether the entity is solvent or not. The firm remains solvent if the total amount of assets results more than total liabilities and if the liabilities exceed assets, then that firm will be considered insolvent.

It helps in preparing the balance of opening entries at beginning of next year.

Grouping of Assets and Liabilities:

When a Firm prepares their accounts, they assemble and present assets and liabilities in a systematic manner. It means showing the items of similar nature under a common heading.

For example, the customers of business who purchased goods and services on credit will be shown under a common name called ‘Sundry Debtors’.

Likewise, Cash, Bank, Stock, etc. will write under Current assets, called ‘Grouping’.

Marshalling of assets and Liabilities:

It refers to process of arranging assets and liabilities in a proper order.

Marshalling can be done in two ways:

In the order of liquidity: In this method, items will be written in ascending order.

An asset that can be easily convertible into cash is written first in the Balance sheet such as cash in hand, cash at bank. After that asset which lies in the middle i.e. which are comparatively less convertible into cash and at last which take time to convert into cash like Furniture, Buildings, etc.

Like the assets, Liabilities also follow the same rule. Liabilities that are to be paid earlier are written primarily such as sundry creditors and Bank overdraft etc. and then the turn of other liabilities.

Generally, Sole proprietors and Partnership Firms apply this method to prepare their Balance sheet.

In order of Permanence: This method is completely reverse of the first method.

As the assets which are most difficult to convert into cash is firstly written such as goodwill, Furniture, Building etc. The assets which are most liquid ( Easy to convert ) are written on the last.

Similarly, those liabilities will be written at first which had to be paid at last such as proprietor’s capital, Long term loans, etc. and current liabilities at the last like sundry creditors.

Joint-stock companies require to prepare their Balance sheet under the Companies Act.

If a Business wants to prepare their Balance sheet under any method, they need to learn the Classification of various assets and liabilities.

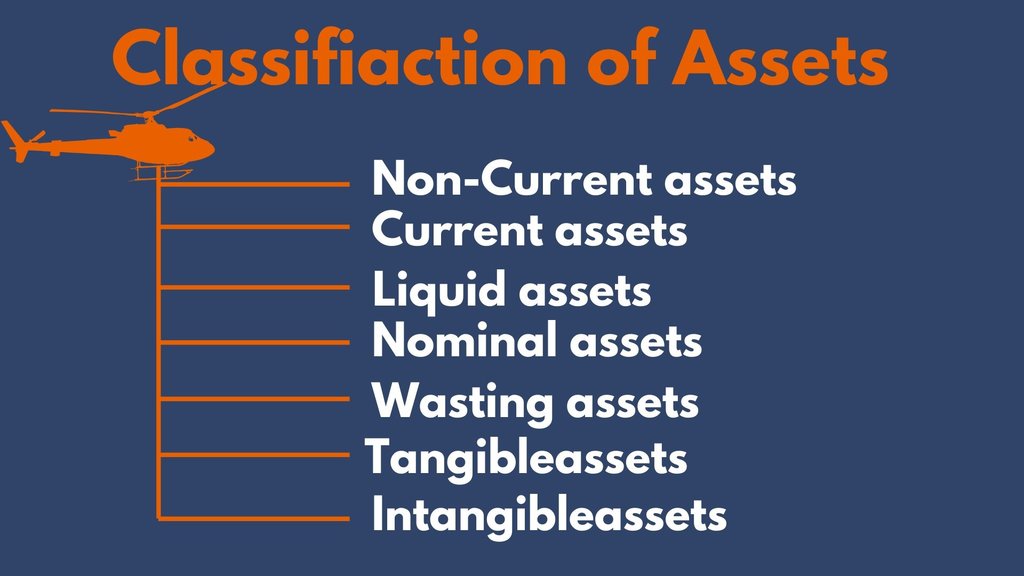

Classification of Assets

- Non-Current Assets

- Current Assets

- Liquid assets

- Fictitious or Nominal Assets

- Wasting Assets

- Tangible Assets

- Intangible Assets

Non-Current Assets:

These are the assets which a Business purchases for continuous use and last for several years. Life span is considered for more than one year. For example, Building, Furniture, Land, Machinery etc.

Firms purchase these assets for the purpose of production not for resell. Changes in market value is ignored and shown in balance sheet at their book value less depreciation.

Current assets:

It refers to those assets which are either in the form of cash or which can be easily converted into cash within one year from the Balance sheet.

For example, Cash in Hand, Cash at Bank, Bill receivables, Debtors, Prepaid expense, Accrued income, and Closing stock, etc. Closing stock always valued at cost or reasonable value whichever results in less.

Liquid Assets:

Assets that are either in the form of cash or can be realized easily. For example, Cash, Bills receivables, Sundry Debtors etc.

| Liquid assets= Current assets – Closing stock – Prepaid expenses |

Fictitious or Nominal assets:

These are the assets which can not be realized in cash or no further benefit can be derived from those assets.

These assets include debit balance of Profit & Loss A/c or the expenditures not yet written off such as advertisement expense.

These assets are not really assets but are shown on the asset side for the purpose of written off every year.

For example, a firm makes a budget of 5 cr. for an advertisement for five years and pay the whole amount at first.

So now 1 cr. is transferred into Profit & Loss A/c and the remaining balance of 4 cr. will be shown on the asset side and transferred every year into Profit & Loss A/c.

Wasting Assets:

These types of assets are exhausted or consumed over a period of time like mines, petrol, energy, etc. Their values decrease with the period of time. This also includes Patents or Properties taken on the lease.

Tangible Assets:

These are the assets that can be seen, touched, or can be felt and have a physical existence. like Plant, Machinery, Furniture, Motor vehicles etc.

Intangible assets:

These assets are the reverse of Tangible assets i.e. which doesn’t have any physical existence. These assets cannot be seen, touched or felt such as Goodwill, patents, Trademarks etc.

Intangible assets are given much value as tangible assets because they also help in earning a profit, such as Goodwill which helps an entity by attracting customers.

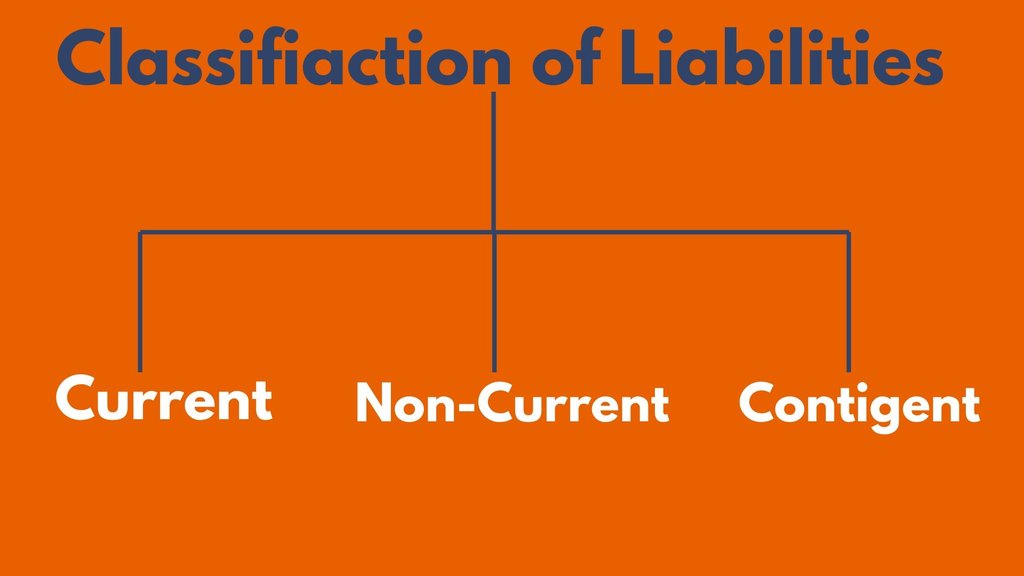

Classification of Liabilities

- Non-current Liabilities

- Current Liabilities

- Contingent Liabilities

Non-current Liabilities:

These are the liabilities that become mature after one year or more than one year i.e. which are to be paid after a year or more. For example, public deposits, Debentures, Capital etc.

Current Liabilities:

These liabilities are expected to be paid within one year from the date of the Balance sheet. This includes, Bills payables, Creditors, Bank overdraft, outstanding expense etc.

Contingent Liabilities:

It refers to those liabilities which is not yet decided to pay or these liabilities become payable only on the happening of some event, otherwise not.

Some of the examples are:

Liability for bill discounted: In some cases, a bill discounted from the bank is dishonored by the acceptor on the due date and the firm is liable to pay that amount to the bank.

Case pending in a court: This would become an actual liability for the firm if the case results against the firm.

Liability in respect of Guarantee given for another person: A firm is liable to pay if a person for whom the guarantee is given is unable to meet his promise.

*Contingent Liabilities are not shown in the balance sheet. They are shown by making a footnote if there is any.*

Conclusion

So in this, we learned all types of assets and liabilities which are essential to know before preparing Balance sheet and also some importance.

If you are a student and accountant then you must know about all this because this is termed as the snapshot of the business i.e. tells the summary of position of Business.

Must read: How to became certified C.A in 5 steps.

Content Marketer

{kind=link}